The Illusion of Wealth in Numbers

We live in a world that equates money with wealth. A bigger number in your bank account is supposed to mean you're better off. But this is a kind of nominal value fallacy – assuming that the face value of currency reflects real wealth. Economists call it the money illusion: people tend to view their wealth in nominal dollars, ignoring inflation. In simple terms, we fool ourselves that a dollar today is worth the same as a dollar last year. We cling to numbers on paper while the real value behind those numbers evaporates.

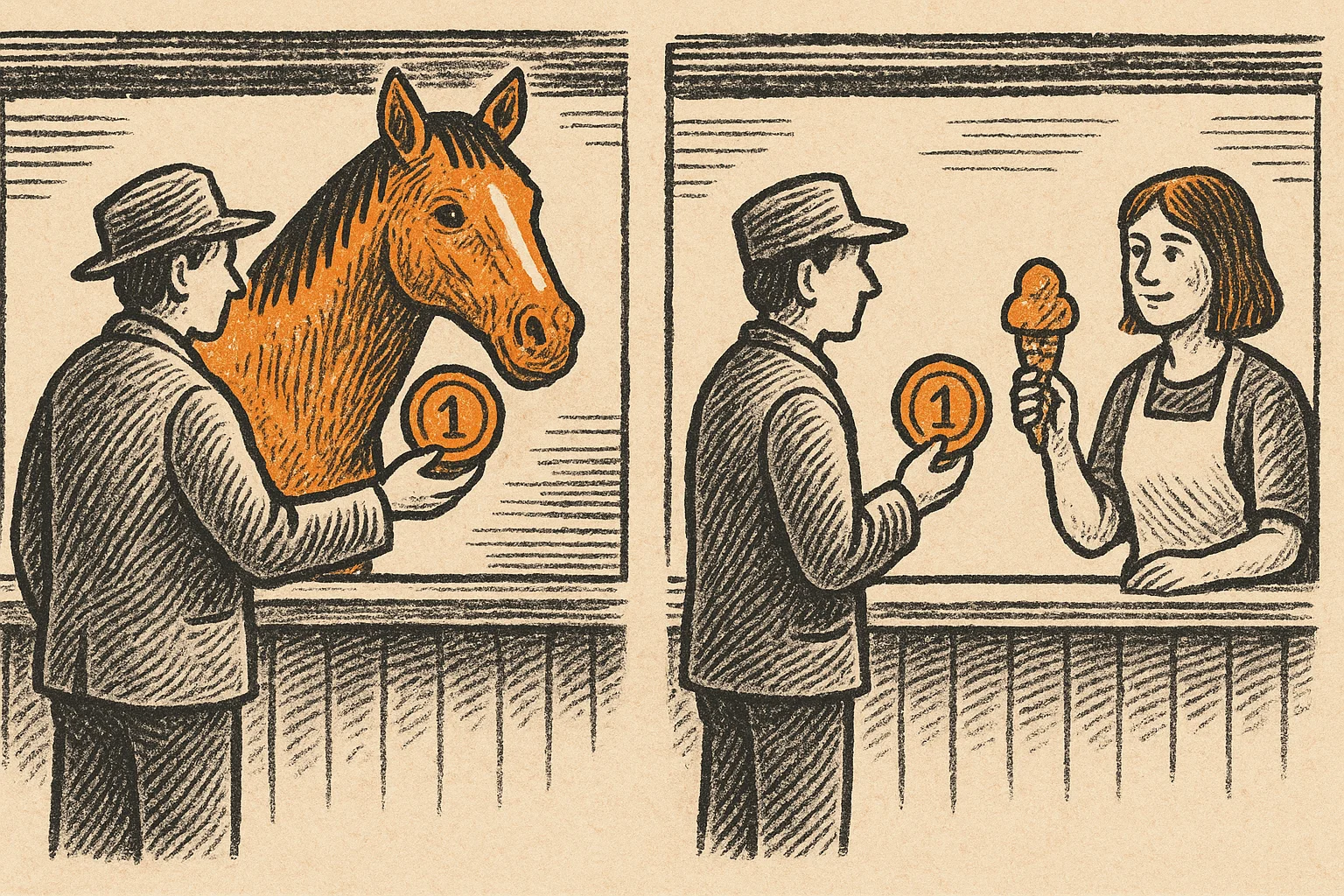

This fallacy didn't happen by accident. Our economic system encourages us to think in terms of currency units. Governments and banks print money, set interest rates, and assure us that a dollar is a dollar. But value isn't an objective substance locked inside a coin or a bill – it's subjective, determined by what someone is willing to give you for that coin or bill. A hundred-dollar bill can buy you a nice dinner today; a century ago it might have bought a horse. Value depends on time, place, and perception. Value is not the number printed on the money – value lives in our minds and in what we can trade for it.

Time: The Ultimate Currency

An hourglass with money reminds us that time is the one currency we can't refill. As time passes, the energy we have to earn and create dwindles, making it ever more vital to preserve the value we earn.

If value is subjective, perhaps the truest measure of value is something we all possess in limited quantity: time. Time is the most precious currency of all. When we're young, we have an abundance of energy and years ahead to work, learn, and build. As we age, that energy fades. Our capacity to trade hours for dollars diminishes. You might say we front-load our working years when we're full of vitality, hoping to store that energy in the form of money for later in life.

But this is where the cruel joke of the system reveals itself. We work hard in our prime years, trading irreplaceable hours of our lives for money – only to watch the value of that money decline over time. Inflation is constantly nibbling at our savings. Prices creep up year after year, and the purchasing power of each dollar declines. In a very real sense, the hours we worked in the past buy fewer hours of comfort in the future. Unless we find a way to make our saved wealth grow faster than inflation, we are running up a down escalator.

Our time is stolen by the subtle lie that a dollar is a stable store of the value created by our labor.

Inflation: When Money Loses Meaning

The hard truth is that most government-issued currencies lose value relentlessly. The U.S. dollar, for example, has lost over 96% of its purchasing power in the last centuryhttps://www.forbes.com.au/news/investing/why-inflation-battered-argentinians-are-turning-to-crypto/. That means if your great-grandfather stashed $100 under a mattress in 1913, its buying power today might be only a few dollars' worth of goods. A number like $100 may stay the same on paper, but what it means in terms of real stuff shrinks dramatically over time.

For those of us who come from places with high inflation, this truth is part of daily life. I grew up in Córdoba, Argentina, and saw firsthand how a currency can betray the people who hold it. Inflation has been as much a part of Argentine identity as our beloved beef barbecues. In the early 2000s, Argentina went through a financial nightmare – the currency collapsed, banks froze accounts, and people's life savings evaporated.

My father learned early that if he saved in Argentine pesos, he was essentially saving ice in the desert sun. By the time I was a child, he refused to hold onto cash for long. He would quickly invest any spare money into something tangible – bricks, literally.

He inherited a piece of land with an old house, and instead of keeping money in the bank, he poured whatever he earned into building small rental units and additions on that land. Real estate, he figured, would hold value better than paper. He was right. Year after year, the peso lost value, sometimes slowly, sometimes in devastating overnight devaluations. In one 12-month stretch recently, Argentina's inflation hit a cumulative 276%. Prices nearly quadrupled, and the cash in people's wallets became nearly worthless. In such an environment, being a "millionaire" in pesos meant nothing – it might buy you a used car, or it might not even buy your family groceries for the month.

My father's strategy was to play a different game: put value into anything but the local currency. He worked brutally long hours, took on side jobs, and even went door-to-door looking for work during the 2001 crisis. He converted sweat into cement, time into tangible assets. Still, it was a rat race.

There were times when despite all the hard work, ends barely met. I remember in 2001 when he lost his steady job, how our family had to tighten our belt. He found a new job in Buenos Aires, and for two years he lived apart from us during the week, traveling 700 kilometers back home on weekends – all that sacrifice just to keep ahead of the tug-of-war between income and rising prices. We eventually moved to the big city to be together, but the routine remained: work hard, save hard, invest in something real, because the money itself was evaporating beneath our feet.

Bitcoin: A Deflationary Lifeboat

In a world of constantly shrinking money, the idea of an inflation-proof currency sounds like a fantasy. That's exactly what Bitcoin set out to be – money that can't be debased by any government or central bank.

Unlike dollars or pesos, Bitcoin has a hard cap on its supply. There will never be more than 21 million bitcoins in existence, a limit written into its code and guarded by a decentralized network of computers around the world. New bitcoins are issued on a predictable schedule that keeps slowing down (a mechanism known as the "halving" that cuts the new supply in half every four years). In other words, Bitcoin is designed to be deflationary – its supply growth will eventually stop, meaning that if demand for Bitcoin increases, its price in terms of fiat currency tends to rise over time.

This built-in scarcity is a radical shift. It means if you hold one bitcoin out of 21 million, you own a fixed slice of all the bitcoin that will ever exist. As more people adopt Bitcoin and demand grows, that fixed slice could represent more and more purchasing power.

Indeed, many people have started to treat Bitcoin as "digital gold," a safe-haven store of value to protect their wealth from currency devaluation. Companies like MicroStrategy and even countries like El Salvador have bought into Bitcoin for this reason. The idea is simple: hold hard money that no one can dilute. As trust in fiat fades – whether due to reckless money printing or political instability – people flee to assets that can't be conjured out of thin air. Gold was the traditional refuge; Bitcoin is the new contender.

Holding the same amount of bitcoin over time, therefore, has a very different meaning than holding the same amount of dollars. If the dollar’s value is like ice melting every year, Bitcoin's value is designed to be like a slowly rising sun, growing warmer as adoption spreads.

One friend of mine put it this way: if you own 1 BTC today, you'll still have 1 BTC in ten years – and that might buy a lot more in 2035 than it does today. In a sense, Bitcoin breaks the nominal value fallacy. It exposes the truth that having more units of money isn't what makes you rich – having money that holds its buying power is what makes you rich.

Under an appreciating currency, the relationship between wealth and the number of units you hold flips on its head. Imagine a world where the currency in your pocket gains value each year. Measuring your net worth in that currency becomes tricky, because the yardstick itself is changing.

We might need new ways to measure wealth – perhaps in terms of tangible assets, or percentage of total money supply, or simply in how many years of comfortable living our savings represent. The key point is, when money gets harder (more value-dense), you don't need more of it to preserve wealth. One bitcoin today could be worth ten tomorrow – not because the coin "produced" value on its own, but because its relative scarcity increased as more people sought it.

The Lure and the Risk of Leverage

Recently, a close friend of mine tried to convince me of a clever scheme to beat the system. He's a true Bitcoin believer. His plan: use Bitcoin as collateral to borrow more money, then buy more Bitcoin with that loan.

In financial terms, he wanted to short the dollar – effectively betting that the dollar's value would fall and Bitcoin's price would rise. On paper, it sounds genius: if you're convinced Bitcoin will keep appreciating against fiat, why not leverage that conviction?

For example (in simplified terms), imagine you have 1 BTC. You borrow some dollars against that BTC on an exchange (say 20% of its value, which is a 5x leverage position), then use those dollars to buy more Bitcoin. Now you have 1.2 BTC instead of 1.0, without spending additional money – you just took a loan. If Bitcoin's price goes up, you can sell a bit, repay the loan, and end up with more BTC profit. It's like a high-octane booster for your holdings.

What my friend was proposing is not new – it's basically margin trading dressed up as a Bitcoin strategy. And margin trading is high risk, high reward – it amplifies your gains and your losses.

I had to smile at his enthusiasm, but I also had to caution him (and myself) with some cold facts.

First, borrowing money isn't free. On exchanges like Binance, when you take a loan in USDT (a dollar-pegged stablecoin) against your Bitcoin, you pay interest on that loan. Those interest costs eat into any potential profit. If lots of people crowd into this trade, the borrowing rates can climb higher, making it even less attractive.

Second, and more importantly, leverage is a double-edged sword. Yes, if Bitcoin's price keeps rising, you win bigger. But if Bitcoin's price drops by a certain amount, your collateral (the original BTC) can be liquidated by the exchange. In the 5x leverage example, a 20% price drop could wipe you out. You'd be forced to sell into a crashing market – exactly what you don't want to do.

In such a scenario, you'd end up with less Bitcoin than you started with, defeating the whole purpose. The asymmetry of risk here is glaring: your upside might be, say, a 20% gain in BTC if things go well, but your downside could be losing 100% of your BTC if things go wrong. That's like risking your house to potentially buy a slightly nicer house – not a trade-off many would take if clearly presented.

Lastly, there's a philosophical catch. Bitcoin was invented to remove trusted intermediaries – “not your keys, not your coins,” as the mantra goes. To execute this leveraged strategy, you have to trust an intermediary (an exchange or lending platform) with your Bitcoin as collateral. My friend's plan involved Binance, a large exchange. Yet even big exchanges come with counterparty risk – they can freeze withdrawals, get hacked, or engage in shady practices.

Handing over your hard-earned Bitcoin to an exchange so you can take a speculative loan cuts against the very ethos of financial self-sovereignty that makes Bitcoin attractive in the first place.

I don't judge my friend for seeking creative ways to build wealth. We're all trying to secure our future in an uncertain system. But I see his leverage scheme as a kind of mirage – a tempting vision that could lead him into a desert of risk. If your base assumption is that Bitcoin will appreciate and the dollar will depreciate, simply holding Bitcoin unleveraged already profits from that. You're already "short USD" by holding BTC instead of dollars. Taking on debt and risk to squeeze out extra gains is like flying too close to the sun.

Conclusion: Wealth in the Age of Hard Money

My journey – from watching my father toil to protect our family's livelihood from a feeble currency, to discovering Bitcoin as a new form of money – has taught me some hard truths.

One truth is that wealth is not the same as money. Real wealth is the product of your time, energy, creativity, and foresight. Money is just a tool to store that wealth. And when that tool is flawed – when the currency steadily loses value – the connection between your effort and your reward is severed. You work an hour, earn a dollar, save it, and later find that dollar buys you less than before. It's demoralizing and unjust, but it's the reality in much of the world today.

Another truth is that not all money is created equal. A sound, scarce money that others trust (be it gold, Bitcoin, or some future innovation) can hold value across time and space. Bitcoin's rise is a symptom of a system where people are desperate for a reliable store of value. It's a vote, by millions of individuals, for a different way of measuring wealth – one that doesn't have a hidden leak. Bitcoin's market value is volatile in the short term, but many see in it the long-term promise of stability in purchasing power. It has already become a global store of value for many who seek a hedge against fiat devaluation, and its limited supply and decentralized design give it a resiliency that no fiat currency can match.

Finally, I've learned that smart wealth preservation often means resisting the urge to get too clever. The nominal value fallacy teaches us that chasing bigger numbers is a fool's errand if the value behind those numbers is hollow. In the same way, chasing exotic schemes to multiply money can be counterproductive if they jeopardize the very foundation of your wealth.

Sometimes the smartest move is simple: work diligently, save in the hardest money you can find, avoid unnecessary risks, and let compound interest or natural appreciation do the heavy lifting. For my father in Argentina, that meant buying bricks instead of holding pesos. For many today, it means holding Bitcoin instead of an overprinted currency.

Let me put it plainly: Our time is our life, and our money is the time we've saved. Don't let the illusion of nominal value steal your life out from under you. In a world that confuses numbers with wealth, seek the truth in what money can actually do – the shelter it can provide, the food it can put on the table, the hours of freedom it can grant.

Recognize that a pile of cash that's rotting in value is no treasure at all, and that a smaller pile of something truly sound can be worth a fortune. As we stand at the crossroads of an old financial order and a new one, it's time (our most precious currency) to shed the illusions.

Wealth isn't measured by the numbers in your account, but by the value those numbers represent in your life. And preserving that value – our time, crystallized into assets – is the real financial imperative of our age.